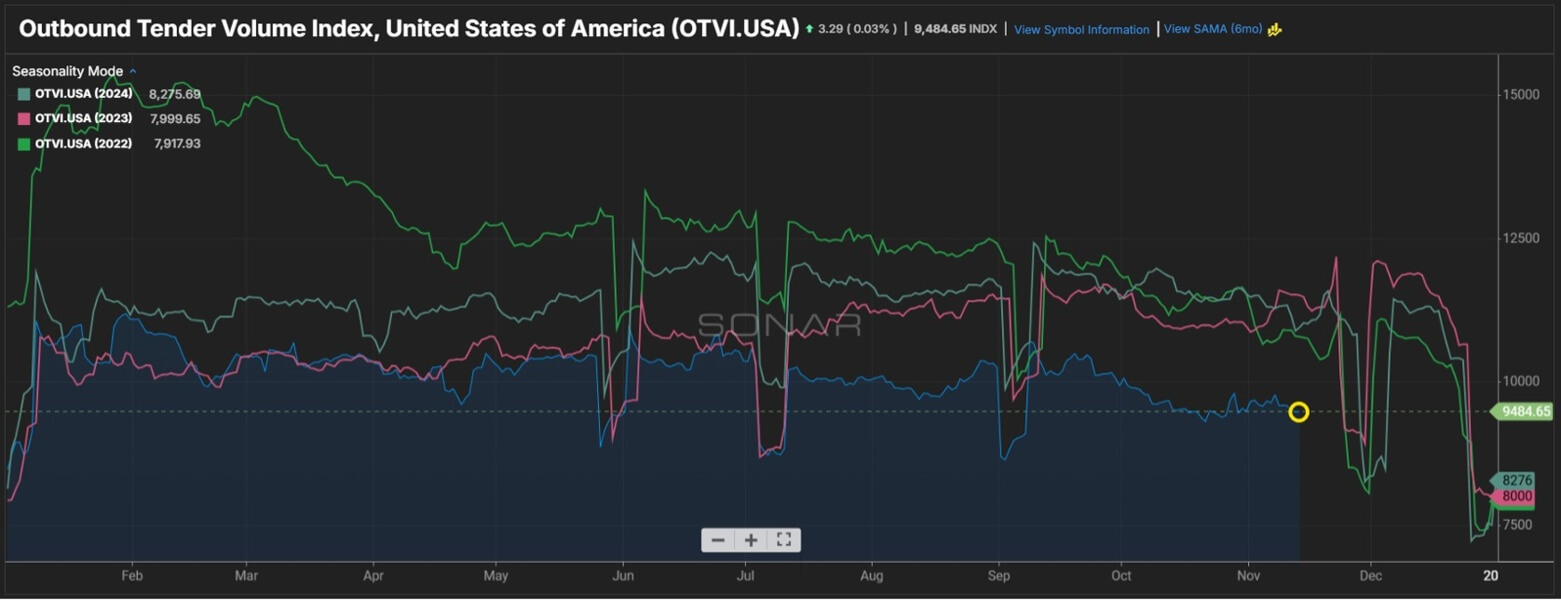

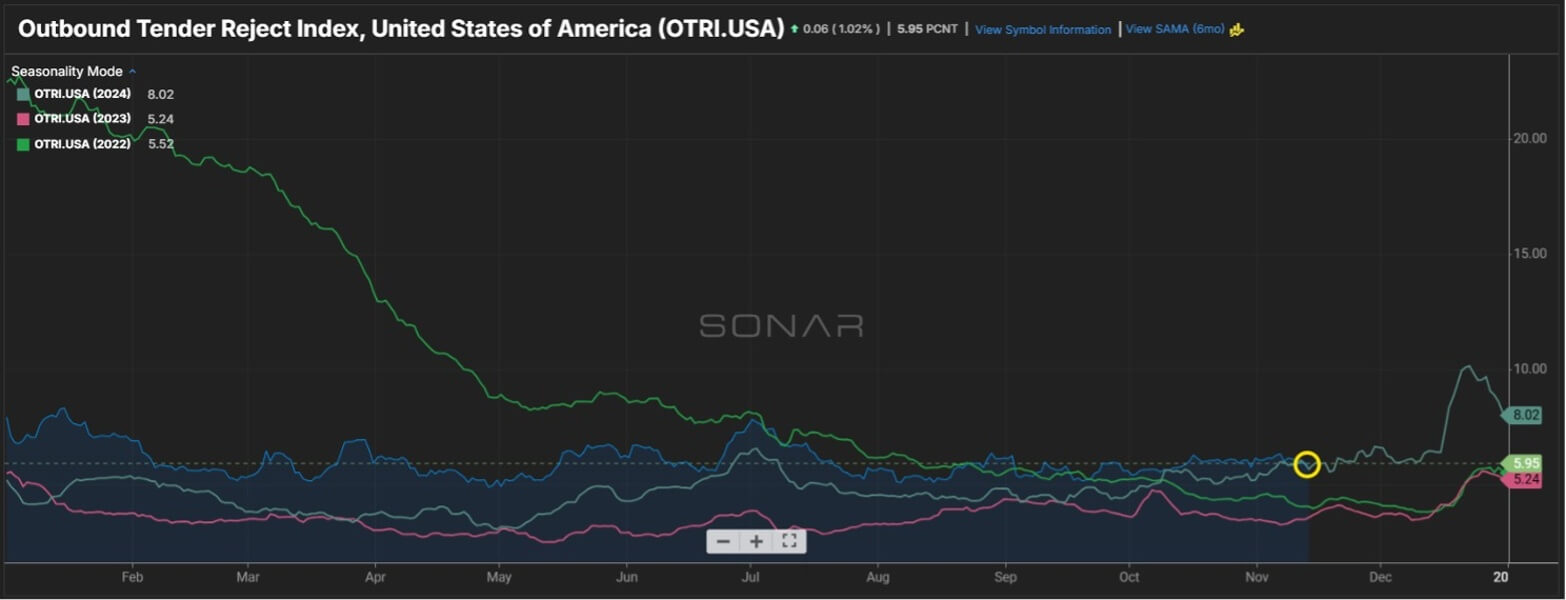

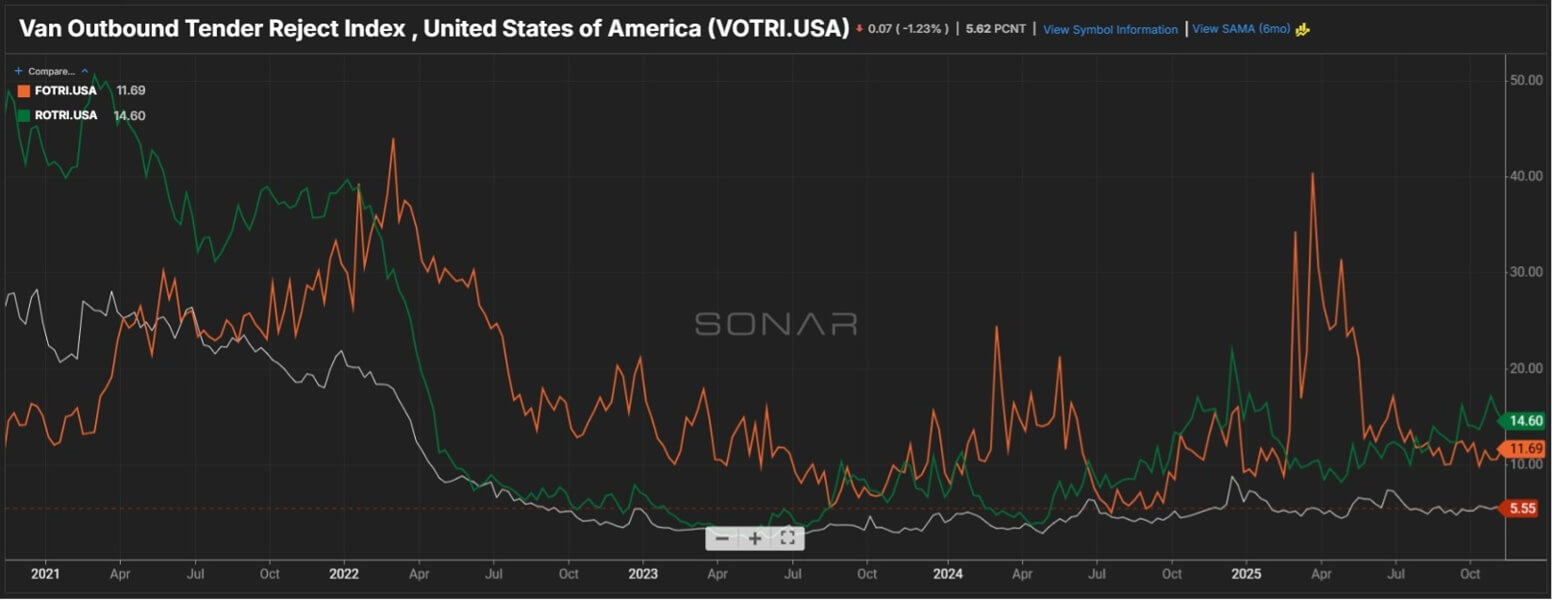

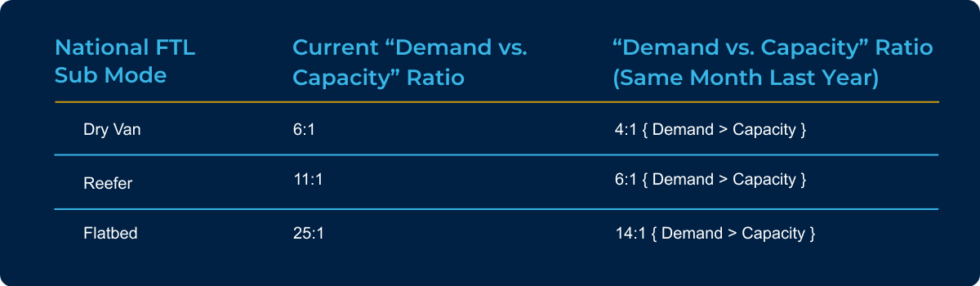

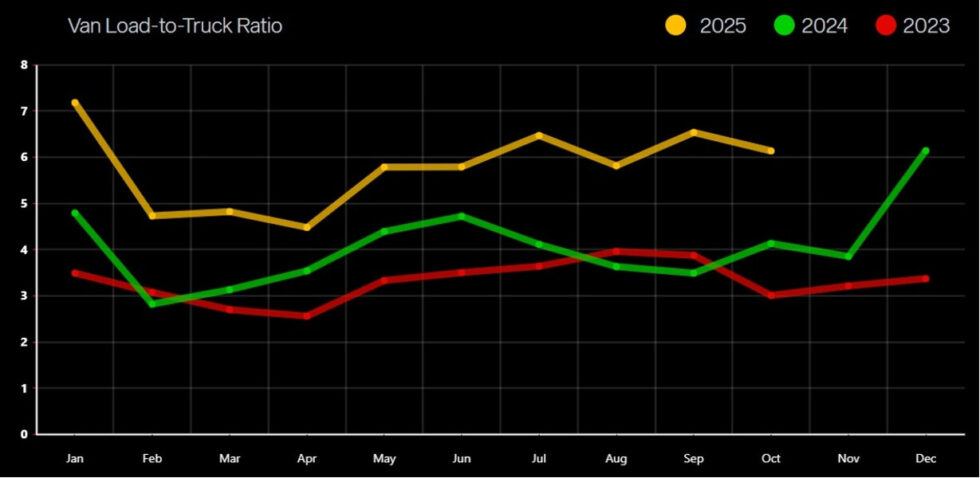

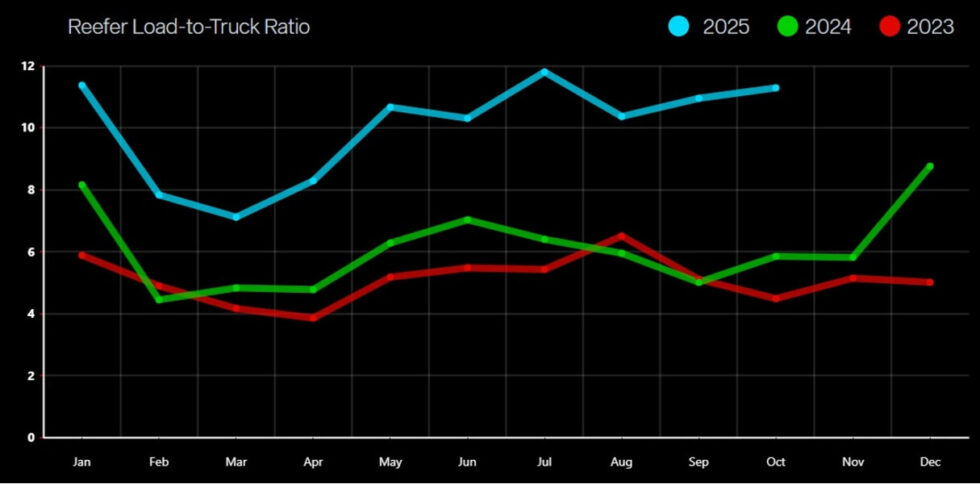

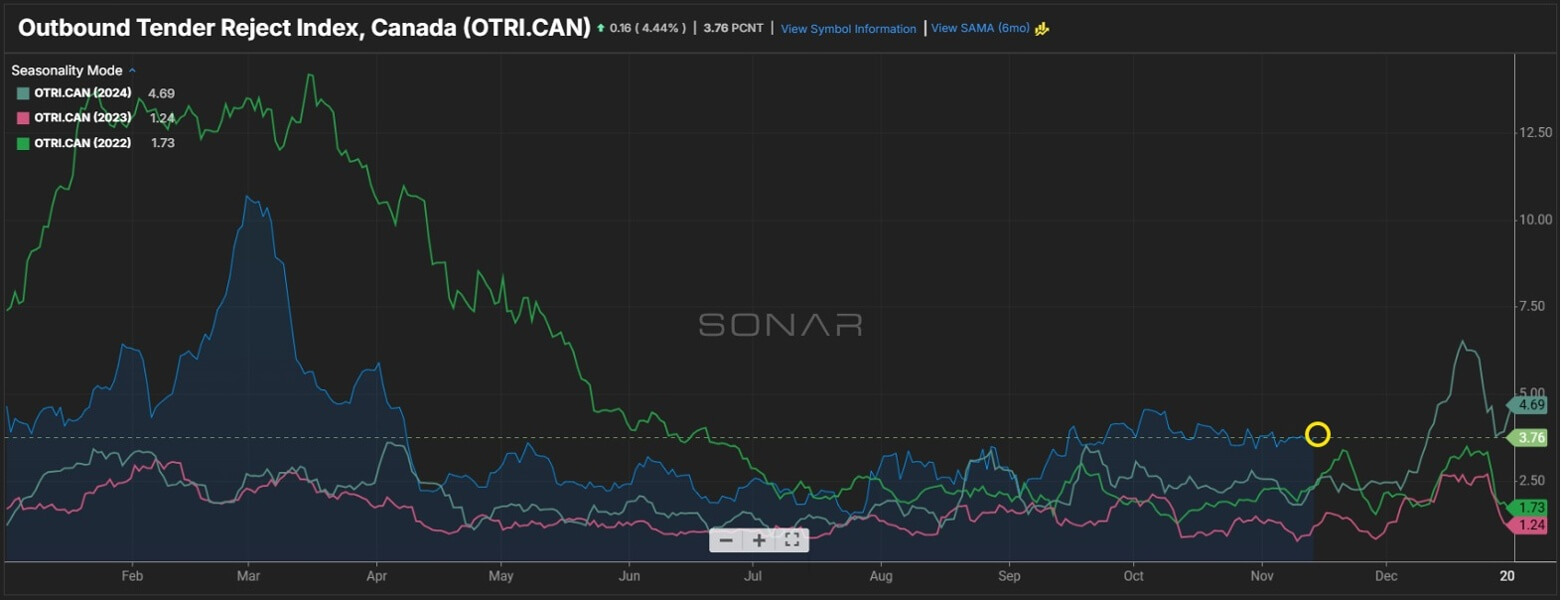

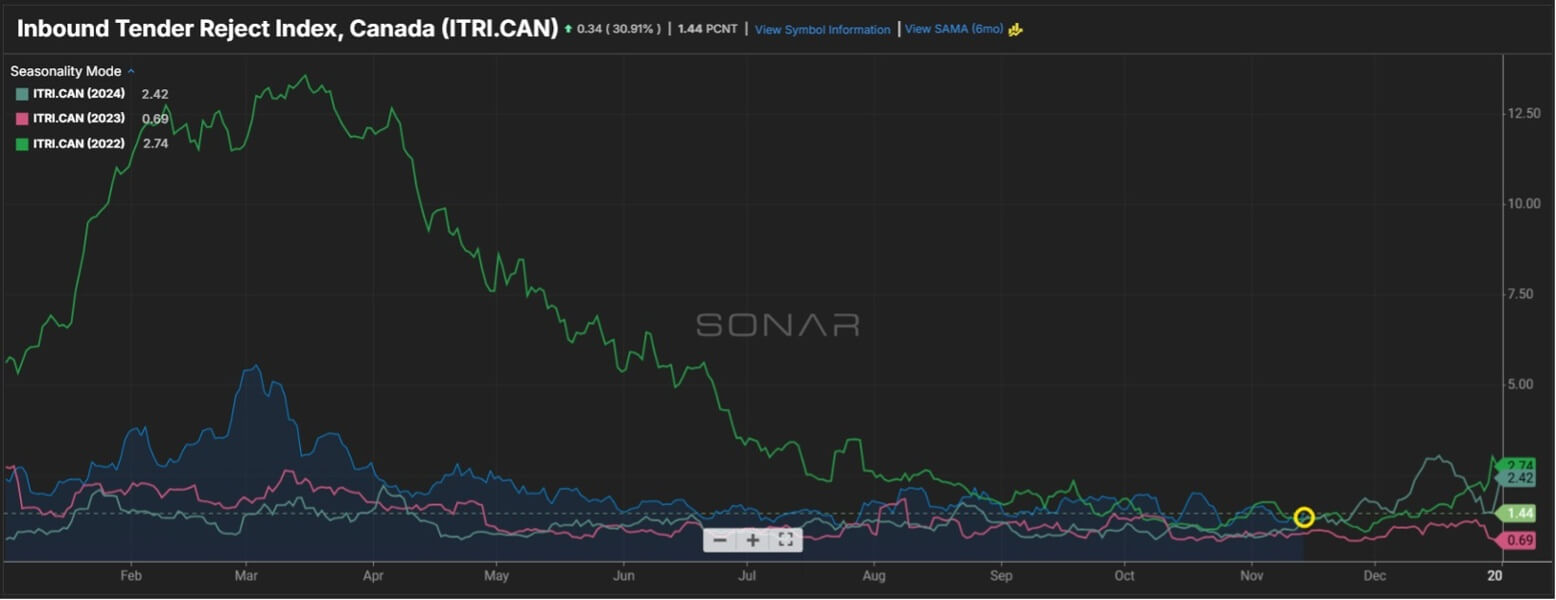

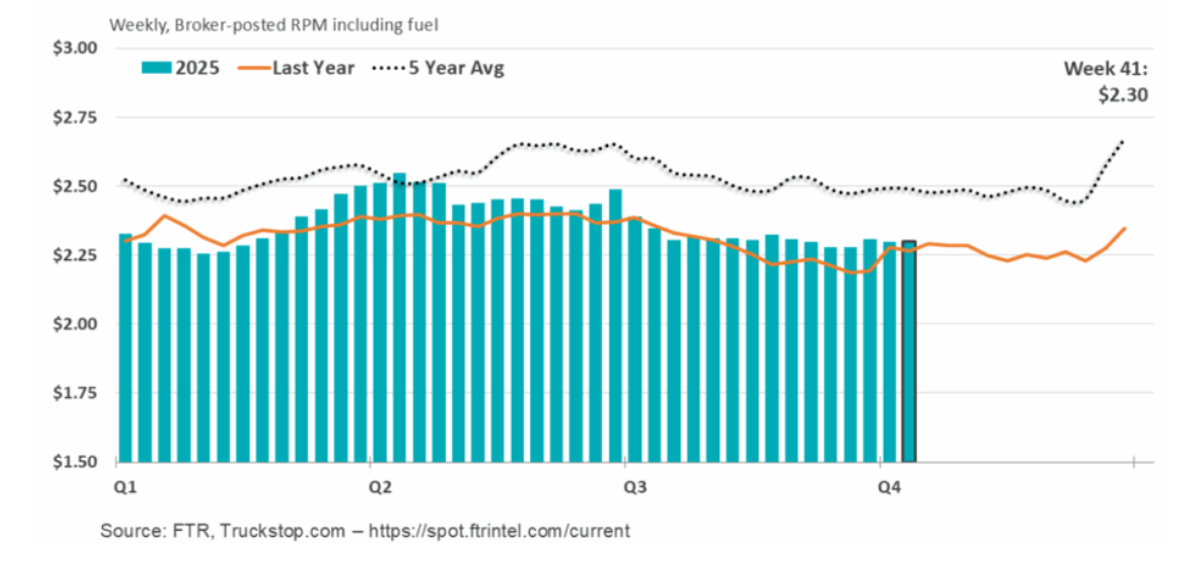

Spot and contract rates continued to trend higher than this time last year. We continueto see capacity tightening and higher rejection rates across the U.S.

During the last month, spot and contract rates continued to remain inflated compared to last year. We continue to see capacity tightening and higher rejection rates across the U.S.

During March, spot rates and contract rates remained inflated vs. last year. We continue to see capacity tightening and higher rejection rates across the U.S.